What Homebuyers and Sellers Need to Know Right Now

The spotlight in the housing market this past week has been firmly on interest rates. With fluctuations across mortgage products, buyers and sellers alike are keeping a close eye on how these changes are shaping affordability and market activity.

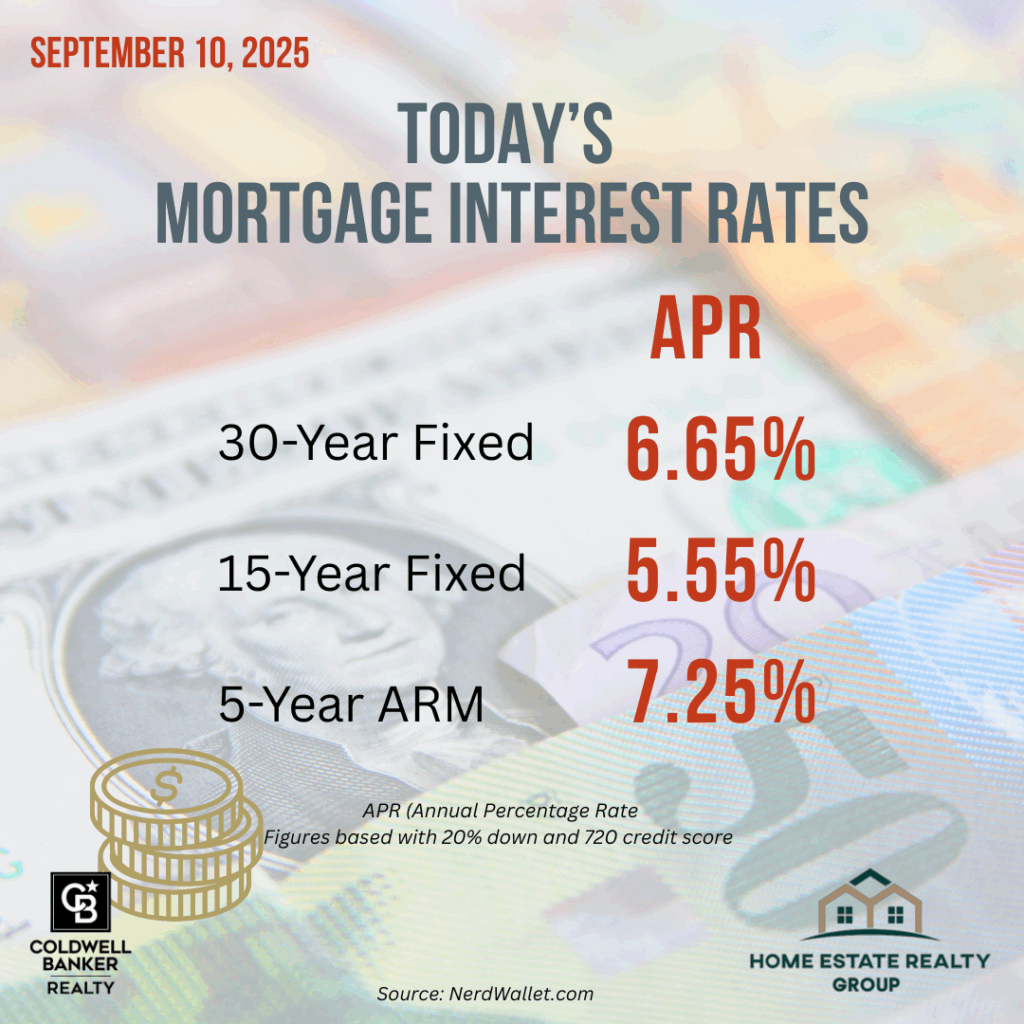

Current Mortgage Rates

As of this week, the average 30-year fixed mortgage rate stands at 6.65%, while the 15-year fixed rate is at 5.55%. Surprisingly, the 5-year ARM has climbed higher, averaging 7.25%, making it less attractive than some fixed-rate options.

Despite these shifts, buyers appear to be adapting. Homes may be spending longer days on market, but properties are still moving — a sign that demand has not disappeared.

Why Rates Are Moving

Several factors are influencing the downward pressure on rates. Key among them:

- Federal Reserve Signals: An upcoming report on September 17 is expected to shed light on the Fed’s next moves. Many analysts believe the federal funds rate could be reduced, likely by a quarter percent.

- Job Market Revisions: Recent job reports have been revised downward, showing weaker conditions than initially reported.

- Inflation Pressures: The Producer Price Index (PPI) suggests inflationary pressure may build later in the fall, especially as tariffs on goods filter through to consumers.

Historically, rate cuts don’t always immediately translate into lower mortgage rates, but expectations are building for at least one — possibly two — reductions before year-end.

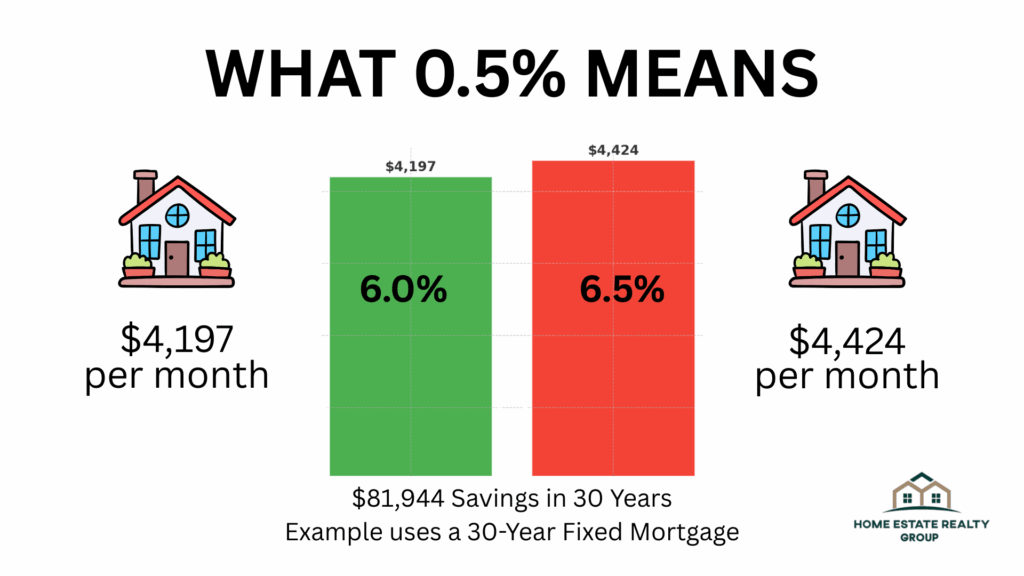

Why a Half-Point Matters

For buyers, even a 0.5% difference in rates can be dramatic. On a $700,000 home with 20% down and strong credit:

- At 6.0%, the monthly payment is about $4,197.

- At 6.5%, the monthly payment rises to $4,425.

- Over 30 years, that difference totals nearly $80,000.

This underscores why it’s critical for buyers to monitor rates daily and work with lenders willing to lock in favorable terms — sometimes for up to 90 days.

Market Implications for Buyers and Sellers

- For Buyers: Lower rates improve affordability, increasing the likelihood of securing more home for the money. More inventory also means opportunities to negotiate contingencies that had been waived in a more competitive market. However, competition is expected to intensify as additional buyers re-enter the market.

- For Sellers: Declining rates bring more buyers into play, increasing traffic and offers. Homes that lingered on the market over the summer may see renewed attention this fall.

The Bottom Line

With rates fluctuating and potential cuts on the horizon, time is of the essence. Buyers may want to act before increased competition drives bidding wars, while sellers could benefit from the wave of renewed demand.

This fall is shaping up to be a potentially robust market for both sides — making it a pivotal moment to watch interest rates closely and move strategically.

Questions? Please contact us.